Buy now, pay later services are retailers’ next great hope

The trend retailer Convey, a shopping mall-society staple, is on a mission to remodel itself for the digital period. It manages a flock of social-advertising influencers and is using details to personalize the knowledge of searching its warm-pink crop tops and sequined assertion blazers. The ending contact on this brand makeover? A partnership with the acquire now, shell out later (BNPL) company Klarna to cobrand digital advertisements and offer Klarna’s “Pay in 4” product—which splits buying-spree expenditures into 4 fascination-cost-free biweekly payments at checkout. “We want to give prospects with a certain perception of us an option to transform that perception,” states Brian Seewald, SVP of e-commerce at Convey. “We’re using the danger out of a order with BNPL,” he suggests, incorporating that Convey prospects who opt to use Klarna have a larger regular-order value.

Obtain now, shell out later solutions, which present buyers a funding remedy and credit rating card option, have been embraced by a lot more than 100 million folks close to the globe in significantly less than a decade. Most BNPL organizations work two shopper products: an fascination-totally free supplying, which breaks up a invest in, generally a lesser-scale transaction, into a few or 4 equal payments and fascination-primarily based installment loans, which unfold out the price tag of much larger buys, like home furnishings. Marketplace leaders Affirm, Afterpay (which Block, formerly Sq., acquired for $29 billion), and Klarna are now ubiquitous on e-commerce websites. Meanwhile, top electronic wallets PayPal and Apple Pay back are pursuing their very own BNPL merchandise. Affirm shares tanked 10% in July of past yr when Bloomberg described Apple’s intention to start a shell out-later product with Goldman Sachs.

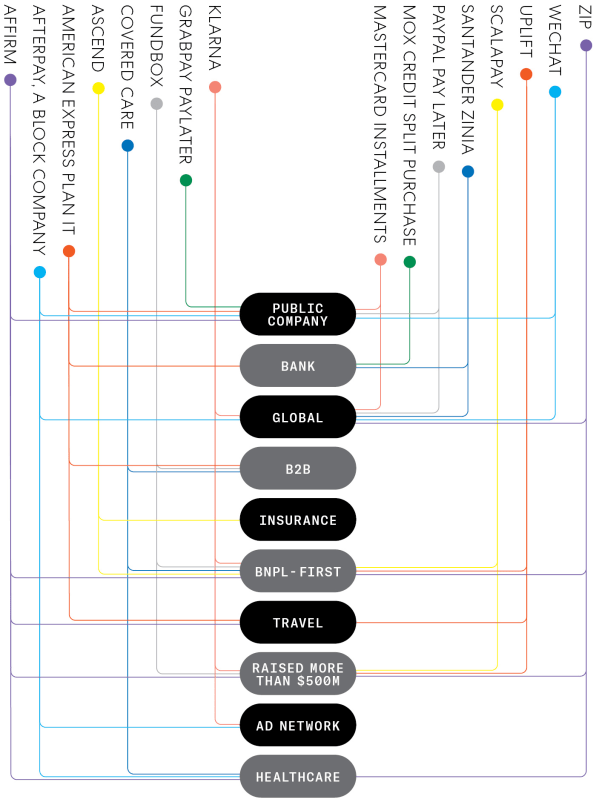

Get, Invest in, Purchase: Mapping the Spreading BNPL Sector

But for vendors like Specific, which aims to arrive at $1 billion in e-commerce profits by 2024, BNPL is not only an extra payment selection for shoppers but also an significantly necessary advertising and marketing tool for suppliers. Klarna is embracing the possibility to assist merchants like Express by proclaiming dollars that may possibly if not have been used on Instagram or other digital adverts. The business, which was valued at $45.6 billion in February, utilizes its application and e mail newsletters to boost spouse brands, taking a smaller slash of any sales opportunities it generates. “We now speak as frequently to the chief advertising officer as we do the head of payments,” says David Sykes, head of Klarna North The usa, “and it is because the benefit proposition has developed.”

Investigation boutique MoffettNathanson estimates that shoppers made use of BNPL to acquire nearly $80 billion in products globally in 2020, $20 billion in the U.S. by itself. In a nod to the sector’s growing prominence, the 3 big credit score companies have reported they will include BNPL payment histories by the finish of the calendar year and the Customer Fiscal Protection Bureau, which is in the midst of an inquiry into the probable for BNPL to be applied for data harvesting and guide to larger financial debt, amid other problems, may well pick out to weigh in on credit-reporting specifications.

Until now, the dominant narrative outlining BNPL’s achievements is that consumers—particularly, younger ones—are hungry for financing alternatives that are considerably less predatory than credit rating cards with their 15% average APR. But there is a lot more to the story. Due to privacy variations, most notably the tracking constraints that Apple built available to Iphone end users in April 2021, retailers have not been in a position to target consumers as a result of platforms like Meta, which owns Fb and Instagram, as they had just before. Nor can they definitively attribute an e-commerce sale to a digital advertisement. BNPL providers, many thanks to their increasingly sturdy applications and e mail lists, can remedy both those troubles. Additionally, they have an edge more than social media and electronic promoting in being familiar with consumers’ credit, and, by extension, their buying energy. Even as they undercut credit cards, BNPL businesses are, by design, amplifying buyer investing. Consumers can still get a fair deal with BNPL merchandise, furnished they stay in their budgets and fork out on time. But they must fully grasp who BNPL providers are really doing work for.

In its early days, in the mid-2010s, BNPL had a comparatively straightforward work. By supplying to split a invest in into month to month payments at the level of sale, BNPL could cut down cart abandonment, a prevalent challenge for larger-ticket things, specifically those people becoming marketed by startup brands these types of as Casper Rest and Peloton. Leading BNPL gamers assert that they can improve checkout conversion premiums by 20% to 30%. “We are in the enterprise of bringing [merchants] new consumers, expanding their cart sizing, increasing their conversion at point of sale,” Affirm cofounder and CEO Max Levchin claimed final year.

That main promise—that customers will spend more—is continue to at the heart of the product’s attraction to merchants. Florist UrbanStems, for example, suggests that buyers who fork out with Affirm shell out $7 more per order on average. Stores have been willing to shell out BNPL organizations about 5% to 6% for every transaction for that raise, somewhere around double what they spend to system credit score card transactions. “It’s beautifully measurable, and that’s why [merchants] are eager to pay out a top quality,” suggests MoffettNathanson companion Lisa Ellis. She likens BNPL to a modern updating of a retail store credit score card. “You occur for the funding, but you remain for the advertising and marketing.”

BNPL gamers are following the retail outlet-card playbook, but with applications and e-mails replacing mailers and “friends and family” revenue. Afterpay, which originates just one-3rd of its transaction quantity by means of its personal app, released a pay-for-performance advertisement system last August. Nick Molnar, Afterpay’s cofounder and coCEO, claims Afterpay Ads, as it’s identified as, is developed to help merchants determine customer groups exactly where they’re underperforming. Now that Afterpay’s merger with Block is full, “taking commerce into Dollars Application will become very intriguing,” he claims, referring to Block’s banklike featuring, which has 44 million customers that Afterpay can current market to.

Afterpay will have enterprise, as competitors glance to establish present day, electronic malls of their individual. Try out BNPL as soon as, download an app to keep track of your payments, and abruptly you are acquiring notifications about can not-pass up promotions. Affirm claims that its buying app has produced more than 10 million referral clicks to service provider web pages. PayPal, the most

significant of the diversified BNPL players, has also began leaning into e-commerce in 2019, it obtained Honey, a purchasing-and-benefits system, for $4 billion.

David Oksman, VP of internet marketing and e-commerce at Samsonite, a PayPal companion, is anticipating a “cookie-fewer future”—meaning that people bits of code utilized to track individuals on line will be no a lot more. He believes that applications like PayPal’s Pay back in 4 can make purchaser loyalty, and has been experimenting with BNPL mentions on social media. “Like everybody else,” he says, “we are looking at new channels.”

“The most new modify with Apple and their advertising and marketing monitoring is probably heading to end up currently being a footnote in what is continuing to be a elementary pivot in promotion on-line,” Affirm CFO Michael Linford explained to traders at a Citi fintech convention final November. “Merchants are getting squeezed.”

By February, that “footnote” was searching additional like a chapter heading soon after Meta forecast that Apple’s privateness adjustments would minimize its 2022 profits by $10 billion. The announcement available a peek at the bucks that will be obtainable to BNPL firms, which master the dim arts of electronic marketing, but also served as a reminder that BNPL startups are participating in an individual else’s match, with minimal power to set the policies.

Apple and Goldman have saved silent about their likely BNPL plans (and declined to break their silence for this story). But Apple’s ability to ascertain irrespective of whether it desires to just take the route that Affirm, Klarna, and other individuals are pursuing is as profound as it was in kneecapping Meta’s advertisement organization. Take into account this:

In 2021, Apple Pay processed an believed $90 billion in transactions for U.S. merchants. If Apple converted even a single-digit share of that total to “Apple Pay Afterwards,” it would declare a sizable slice of BNPL enterprise for itself—in 1 quick installment.